Interest rate vs annual percentage rate

In the realm of financial matters, especially loans, you often encounter terms like “interest rate” and “Annual Percentage Rate (APR)”.

They hold the key to understanding the cost of borrowing. However, confusion often arises between these terms.

So, what are interest rates? And what is the annual percentage rate? What’s the relationship between these two terms, and above all, how do they differ?

In this article, you will learn more about interest rates and APRs and discover their differences.

You will also clarify their importance and how they affect your eligibility for personal loans.

Interest Rate: Getting the Basics Right

An interest rate refers to the percentage of the borrowed amount that a lender charges you for borrowing money.

Simply put, it’s the cost you pay for taking out a loan. This rate is calculated as a percentage of the total loan amount.

The interest rate has a significant impact on your monthly payments.

A higher interest rate increases your monthly payments, which means paying more over the life of your loan.

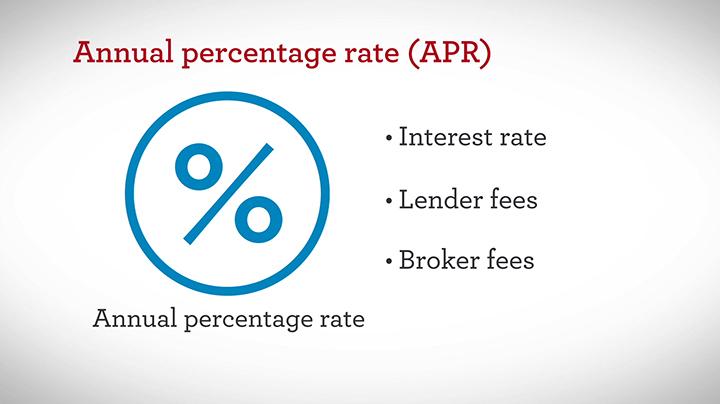

Annual Percentage Rate (APR): Unveiling Complexity

Enter the Annual Percentage Rate (APR)—a more comprehensive measure. It does not only include the interest rate but also considers additional fees or charges associated with the loan.

Think of it as a fuller picture of your borrowing costs. That could comprise origination fees, processing charges, and other related borrowing costs.

While interest rates are straightforward, APR can seem more intricate due to the inclusion of these extra fees.

Key Differences

1. Factoring in Fees

The primary difference between interest rates and APR lies in what they account for.

While an interest rate reflects just the borrowing cost, the APR goes beyond and covers both the interest rate and any extra fees.

Consequently, the APR usually turns out to be higher than the interest rate.

2. Comparing on Equal Ground

APR serves as your tool for a like-for-like comparison between various loan options.

With lenders offering different terms and fee structures, solely comparing interest rates can lead you astray.

The APR creates a level playing field, allowing you to gauge the total cost of borrowing accurately.

3. Impact on Personal Loan Eligibility

Your eligibility for a personal loan depends on factors like credit score, income, and existing debts.

While both; the interest rate and APR play roles here, the APR might exert a more significant influence.

Lenders use the APR to assess repayment ability, considering the entire borrowing cost.

Understanding the Significance

Imagine you’re considering two loan offers. One boasts a lower interest rate, while the other presents a higher interest rate but a lower APR.

While the lower interest rate might attract you initially, the higher APR loan could actually be the more cost-effective choice due to lower additional fees.

And this is where the APR comes to your rescue—helping you make an informed decision based on the complete borrowing expense.

Personal Loan Eligibility and APR

For personal loan eligibility, lenders assess your financial standing and creditworthiness to decide if you’re fit for the loan.

While the interest rate matters, the APR also has its say. A higher APR indicates a pricier borrowing journey, which could impact your ability to manage monthly payments comfortably.

Lenders use the APR as a way to safeguard against borrowers biting off more than they can chew. This concern is particularly prominent in personal loans, where you have more flexibility in using the funds. A higher APR might raise questions about your capability to handle the loan responsibly, potentially impacting your eligibility.

Conclusion

Interest rates and Annual Percentage Rates (APRs) are connected yet distinct players in the borrowing arena. Interest rates depict the principal borrowing cost, while APRs comprise not just the interest rate but additional fees, too.

That offers a holistic view of your borrowing expenses. Whether you’re comparing loan options or evaluating personal loan eligibility, the APR is your go-to metric, ensuring you make decisions grounded in the complete financial picture.

Whether you’re eyeing a personal loan, a mortgage, or any other form of credit, understanding the differences between interest rates and APRs empowers you to navigate the borrowing landscape skillfully.

While the interest rate is crucial, remember the APR’s significance—it reveals the actual cost of borrowing and holds sway over your loan eligibility.